A beginner’s guide to investing PDF serves as a foundational resource for individuals looking to navigate the world of investment strategies and financial planning. CONDUCT.EDU.VN offers comprehensive information on various investment vehicles, providing guidance on risk assessment, asset allocation, and long-term financial goals. Dive into our expertly crafted content to find a reliable wealth management handbook and discover the keys to smart investment portfolios, along with essential tips and tricks for success.

1. Opportunity Zones Explained: A Comprehensive Overview

Opportunity Zones represent a transformative initiative designed to spur economic development in designated communities across the United States. These zones, established under the 2017 Tax Cuts and Jobs Act, offer significant tax incentives to investors who reinvest their capital gains into Qualified Opportunity Funds (QOFs). A QOF is an investment vehicle structured to invest in businesses and properties located within these zones. This initiative aims to stimulate economic growth and job creation in underserved areas by channeling private capital into projects that might otherwise struggle to attract funding.

The Opportunity Zone program is the most significant economic development program in the U.S. history, according to the Economic Innovation Group. This is because it’s not just about tax breaks; it’s about fostering sustainable economic growth and community development. By incentivizing long-term investments, the program aims to create a ripple effect of positive change, including increased property values, new business ventures, and improved quality of life for residents.

Investing in Opportunity Zones is not just about financial gain; it’s about making a positive impact on communities that need it most. This dual benefit of financial and social returns makes Opportunity Zones an attractive option for investors looking to align their investment strategies with their values.

2. Understanding Opportunity Zone Tax Benefits

The primary allure of Opportunity Zones lies in the substantial tax advantages they offer to investors. By reinvesting capital gains into a Qualified Opportunity Fund (QOF), investors can unlock a trifecta of tax benefits:

- Temporary Deferral: The initial capital gain is deferred until the earlier of the date the Opportunity Zone investment is sold or December 31, 2026.

- Basis Reduction: If the Opportunity Zone investment is held for at least five years, the basis of the original capital gain is reduced by 10%. If held for at least seven years, the basis is reduced by an additional 5%, for a total reduction of 15%.

- Permanent Exclusion: If the Opportunity Zone investment is held for at least ten years, any capital gains accrued from the QOF investment itself are permanently excluded from taxation.

These tax benefits are designed to encourage long-term investment in Opportunity Zones, providing a significant incentive for investors to commit their capital for at least a decade. The ability to defer, reduce, and potentially eliminate capital gains taxes makes Opportunity Zones an unparalleled investment opportunity for those seeking to maximize their returns while contributing to community development.

Example of Tax Benefits:

Let’s illustrate the potential tax benefits with an example. Suppose an investor has a $1 million capital gain and reinvests it into a QOF within the required 180-day period.

- Deferral: The $1 million capital gain is deferred until December 31, 2026.

- Basis Reduction: If the QOF investment is held for seven years, the basis is reduced by 15%, resulting in a taxable gain of $850,000 when the deferred gain is recognized.

- Permanent Exclusion: If the QOF investment is held for ten years and appreciates to $2 million, the $1 million gain from the QOF investment is permanently tax-free.

This example demonstrates the powerful potential of Opportunity Zones to not only defer and reduce taxes but also to eliminate them entirely on long-term gains. It’s important to consult with a tax advisor to understand the specific implications of Opportunity Zone investments for your individual financial situation.

3. A Concise History of Opportunity Zones

The genesis of Opportunity Zones can be traced back to a 2015 white paper published by the Economic Innovation Group (EIG), titled Unlocking Private Capital to Facilitate Economic Growth in Distressed Areas. This paper proposed the concept of “Opportunity Zones” as a mechanism to channel private investment into economically disadvantaged communities. The idea gained bipartisan support and was eventually incorporated into the 2017 Tax Cuts and Jobs Act.

The legislation allowed governors of each state to nominate up to 25% of their low-income census tracts as Opportunity Zones, based on specific economic criteria. These nominations were then certified by the U.S. Department of Treasury. The goal was to identify areas that were ripe for investment and had the potential for significant economic growth.

Since their inception, Opportunity Zones have attracted considerable attention from investors, developers, and policymakers alike. The program has been lauded for its potential to revitalize communities and create jobs, but it has also faced scrutiny regarding its effectiveness and potential for unintended consequences. Despite these challenges, Opportunity Zones remain a significant tool for economic development, and their impact will continue to be evaluated in the years to come.

4. Locating Opportunity Zones: A Geographical Perspective

Opportunity Zones are strategically located in diverse communities across the United States, encompassing urban, suburban, and rural areas. They can be found in every state, major city, and overseas territory, accounting for approximately 12 percent of the nation’s landmass. This widespread distribution ensures that investors have a wide range of options when selecting projects and locations for their Qualified Opportunity Fund (QOF) investments.

The U.S. Department of Housing and Urban Development (HUD) provides detailed maps and resources to help investors identify Opportunity Zones in specific areas. These resources typically include interactive maps, demographic data, and economic profiles of each zone, allowing investors to make informed decisions based on their investment goals and risk tolerance.

Key Considerations When Evaluating Opportunity Zone Locations:

- Demographics: Understanding the population size, income levels, and educational attainment of residents in the Opportunity Zone is crucial for assessing the potential for economic growth.

- Infrastructure: The availability of transportation, utilities, and other essential infrastructure can significantly impact the viability of development projects.

- Local Government Support: A supportive local government that is committed to attracting investment and streamlining the permitting process can be a valuable asset.

- Existing Businesses: Analyzing the existing business landscape in the Opportunity Zone can provide insights into potential opportunities for collaboration and expansion.

By carefully evaluating these factors, investors can identify Opportunity Zone locations that offer the greatest potential for success.

5. Navigating Opportunity Zone Investments: Two Primary Approaches

There are generally two primary approaches to investing in Opportunity Zones, each catering to different levels of investor involvement and expertise:

1. Active QOF Investment: This approach involves the investor taking a hands-on role in managing the Qualified Opportunity Fund (QOF) and the underlying projects. This is often the preferred route for investors who have realized a capital gain and wish to actively manage their next investment as a general partner (GP). In this scenario, the investor creates their own QOF and uses it to fund a property, business, or portfolio of assets within the Opportunity Zone.

2. Passive QOF Investment: This approach is more suitable for investors who prefer a “hands-off” approach. In this case, the investor invests in an existing QOF that is managed by a professional fund manager. This allows the investor to benefit from the tax advantages of Opportunity Zones without having to actively manage the investment.

Comparison of Active vs. Passive QOF Investments:

| Feature | Active QOF Investment | Passive QOF Investment |

|---|---|---|

| Management | Investor actively manages the QOF and underlying projects | Professional fund manager manages the QOF |

| Involvement | Requires significant time and expertise | Requires minimal time and involvement |

| Control | Investor has full control over investment decisions | Investor has limited control over investment decisions |

| Risk | Higher risk due to direct involvement in management | Lower risk due to professional management |

| Potential Return | Higher potential return due to active management | Lower potential return due to management fees |

| Suitability | Suitable for experienced investors with the time and expertise to actively manage investments | Suitable for investors who prefer a “hands-off” approach and want to diversify their portfolio |

Choosing the right approach depends on the investor’s individual circumstances, investment goals, and risk tolerance.

6. Investing in Opportunity Zone Funds: A Step-by-Step Guide

Investing in Qualified Opportunity Funds (QOFs) typically involves a process that differs from traditional investments in publicly traded stocks or bonds. QOFs are generally private placement funds, meaning that their shares or interests are not available on public exchanges. Instead, they are more akin to private equity funds or private real estate funds.

Here’s a step-by-step guide to investing in Opportunity Zone Funds:

- Identify a Capital Gain: The first step is to identify a qualifying capital gain, such as the sale of stock, real estate, or a business.

- Understand the Timeline: You have 180 days from the date of the sale to invest the capital gain into a QOF.

- Research QOFs: Conduct thorough research to identify QOFs that align with your investment goals and risk tolerance. Consider factors such as the fund manager’s experience, the fund’s investment strategy, and the types of projects the fund intends to invest in.

- Review Offering Documents: Carefully review the QOF’s offering documents, including the private placement memorandum (PPM), which outlines the terms and conditions of the investment.

- Consult with a Financial Advisor: It’s always a good idea to consult with a qualified financial advisor who can help you assess the suitability of the investment and understand the potential risks and rewards.

- Complete Subscription Documents: Once you’ve decided to invest, you’ll need to complete the QOF’s subscription documents, which typically include an application form and an investor questionnaire.

- Fund the Investment: After your subscription is accepted, you’ll need to transfer the capital gain to the QOF within the 180-day timeframe.

- Monitor Your Investment: Stay informed about the QOF’s performance and track the progress of the underlying projects.

Key Considerations When Selecting a QOF:

- Fund Manager Experience: Look for fund managers with a proven track record of success in real estate, private equity, or other relevant investment areas.

- Investment Strategy: Understand the fund’s investment strategy and ensure that it aligns with your investment goals and risk tolerance.

- Project Pipeline: Evaluate the quality and potential of the projects that the fund intends to invest in.

- Fees and Expenses: Be aware of all fees and expenses associated with the investment, including management fees, performance fees, and administrative costs.

By following these steps and carefully considering these factors, investors can make informed decisions about investing in Opportunity Zone Funds.

7. Launching Your Own Opportunity Zone Fund: A Practical Guide

Creating a Qualified Opportunity Fund (QOF) can be a rewarding but complex undertaking. Here’s a simplified guide to help you navigate the process:

- Establish a Legal Entity: The QOF must be organized as a corporation or partnership for federal income tax purposes.

- Develop an Investment Strategy: Define the QOF’s investment strategy, including the types of projects it will invest in, the geographic focus, and the target return on investment.

- Draft an Offering Document: Prepare a comprehensive offering document, such as a private placement memorandum (PPM), that discloses all material information about the QOF, including the investment strategy, risks, fees, and terms of the offering.

- Comply with Securities Laws: Ensure that the QOF complies with all applicable federal and state securities laws, including registration requirements or exemptions.

- Raise Capital: Market the QOF to potential investors and raise capital to fund the QOF’s investments.

- Invest in Qualified Opportunity Zone Property: The QOF must invest at least 90% of its assets in Qualified Opportunity Zone Property (QOZP), which includes tangible property used in a trade or business within an Opportunity Zone, stock or partnership interests in a Qualified Opportunity Zone Business (QOZB), or both.

- Maintain Compliance: Continuously monitor the QOF’s compliance with Opportunity Zone regulations, including the requirement to substantially improve tangible property and the working capital safe harbor for QOZBs.

- Report to the IRS: File Form 8996 with the IRS annually to certify that the QOF meets the requirements for Opportunity Zone status.

Key Considerations When Starting an OZ Fund:

- Legal and Regulatory Compliance: Seek legal counsel to ensure compliance with all applicable securities laws and Opportunity Zone regulations.

- Fund Administration: Consider hiring a fund administrator to handle the day-to-day operations of the QOF, including accounting, reporting, and compliance.

- Due Diligence: Conduct thorough due diligence on all potential investments to assess their viability and ensure compliance with Opportunity Zone requirements.

- Exit Strategy: Develop a well-defined exit strategy for the QOF’s investments, including the potential for sale, refinancing, or other liquidity events.

Starting a Qualified Opportunity Fund requires careful planning and execution. By following these steps and seeking expert advice, you can increase your chances of success.

8. Opportunity Zones vs. 1031 Exchanges: A Comparative Analysis

Opportunity Zones and 1031 exchanges are both tax-advantaged investment strategies that allow investors to defer capital gains taxes. However, there are some key differences between the two:

| Feature | Opportunity Zones | 1031 Exchanges |

|---|---|---|

| Eligible Assets | Any type of capital gain, including stocks, bonds, and real estate | Only real estate |

| Investment Location | Must be invested in a Qualified Opportunity Zone | Must be invested in “like-kind” property |

| Holding Period | To maximize tax benefits, the investment must be held for at least 10 years | No minimum holding period |

| Tax Benefits | Deferral, basis reduction, and potential elimination of capital gains taxes | Deferral of capital gains taxes |

| Complexity | More complex due to compliance requirements and limited investment options | Less complex due to established regulations and a wider range of investment options |

| Risk | Higher risk due to investments in economically distressed communities | Lower risk due to investments in established real estate markets |

| Investment Timeline | The gain must be invested in a QOF within 180 days of the sale. | Strict deadlines for identifying and acquiring replacement property (45 days to identify, 180 days to close) |

When to Choose Opportunity Zones:

- You have a capital gain from the sale of an asset other than real estate.

- You are willing to invest in economically distressed communities.

- You are seeking long-term tax benefits and potential for significant appreciation.

When to Choose 1031 Exchanges:

- You are selling real estate and want to reinvest in another property.

- You want to defer capital gains taxes without investing in a specific geographic area.

- You prefer a less complex investment strategy with established regulations.

Both Opportunity Zones and 1031 exchanges can be valuable tools for managing capital gains taxes. The best choice depends on your individual circumstances, investment goals, and risk tolerance.

Appendix: Essential Opportunity Zone Resources for Further Learning

To deepen your understanding of Opportunity Zones, here’s a curated list of resources from OpportunityZones.com, along with additional materials from federal, state, and local governments, as well as national advocacy and economic research organizations:

- OpportunityZones.com: This website provides a wealth of information on Opportunity Zones, including articles, guides, and investment opportunities.

- IRS Opportunity Zones FAQs: The IRS provides a comprehensive set of FAQs on Opportunity Zones, covering topics such as eligibility, compliance, and reporting requirements.

- Economic Innovation Group (EIG): EIG is a bipartisan public policy organization that originally conceived the Opportunity Zone concept. Their website offers research, analysis, and policy recommendations related to Opportunity Zones.

- U.S. Department of Housing and Urban Development (HUD): HUD provides data and resources on Opportunity Zones, including maps, demographic information, and economic profiles.

- State and Local Government Websites: Many state and local governments have created websites dedicated to Opportunity Zones, providing information on local incentives, projects, and investment opportunities.

- National Council of State Housing Agencies (NCSHA): NCSHA provides resources and advocacy for state housing finance agencies, which play a key role in Opportunity Zone development.

By leveraging these resources, investors can stay informed about the latest developments in the Opportunity Zone landscape and make informed decisions about their investments.

More Ways to Explore Opportunity Zones

Comprehensive PDF Guide

For an in-depth exploration of Opportunity Zones, download the full version of Opportunity Zones Explained: The Beginner’s Guide To OZs in PDF format. This comprehensive guide provides a detailed overview of the program, its benefits, and how to invest. Download the full PDF guide

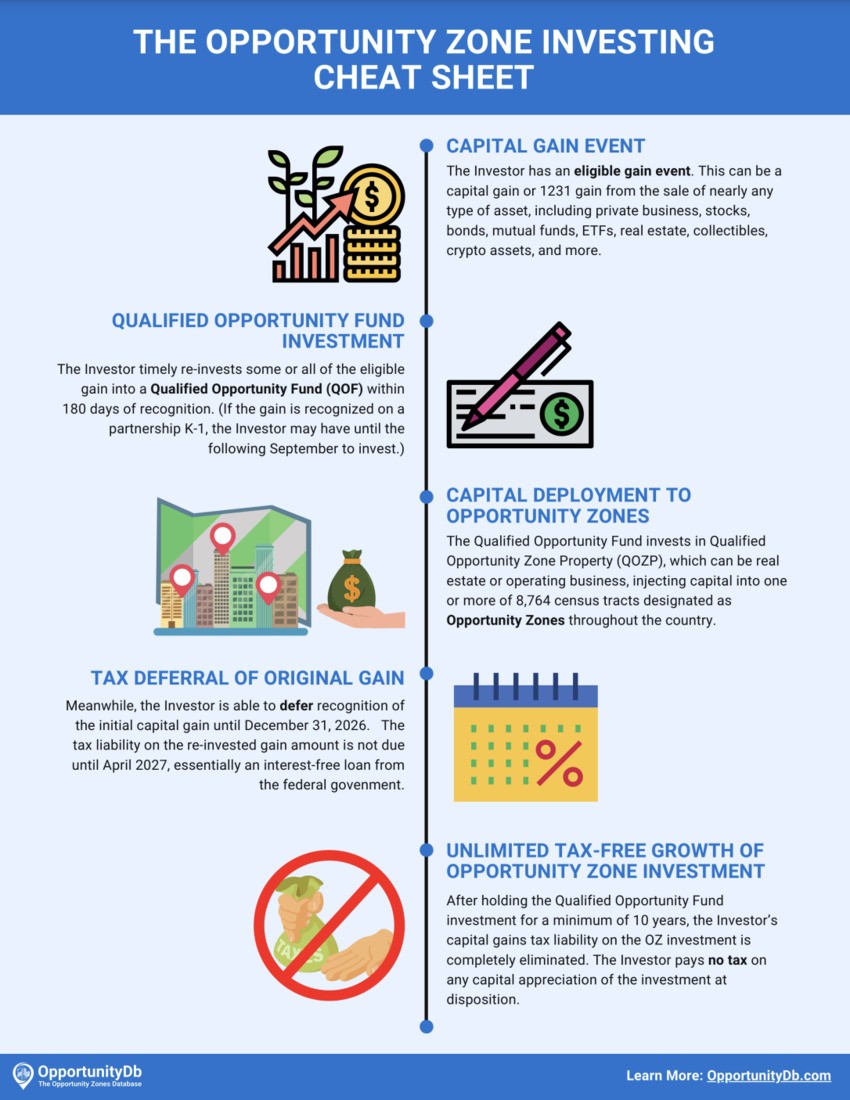

Quick Reference Cheat Sheet

Need a quick refresher on Opportunity Zones? Download The Opportunity Zone Investing Cheat Sheet, a one-page visual explainer of how investing in Opportunity Zones works. This cheat sheet provides a concise overview of the key concepts and benefits of the program.

Download the PDF cheat sheet

Video Crash Course

Prefer learning through video? Watch our 25-minute crash course that’s now available on YouTube. This video provides a visual and engaging overview of Opportunity Zones, covering the key concepts and benefits of the program.

[

Understanding Investment Strategies: A Detailed Guide

Embarking on the investment journey requires a solid understanding of various investment strategies tailored to different financial goals, risk tolerances, and time horizons. Here’s a detailed guide to some of the most common and effective investment strategies:

1. Value Investing

Value investing is an investment strategy that involves selecting stocks that are trading for less than their intrinsic value. Value investors seek out companies that are undervalued by the market and have the potential for long-term growth.

Key Principles of Value Investing:

- Fundamental Analysis: Value investors rely heavily on fundamental analysis to assess the financial health and intrinsic value of a company. This involves analyzing financial statements, industry trends, and competitive positioning.

- Margin of Safety: Value investors seek a “margin of safety” by purchasing stocks at a significant discount to their estimated intrinsic value. This provides a cushion against potential errors in valuation and market volatility.

- Long-Term Perspective: Value investing is a long-term strategy that requires patience and discipline. Value investors are willing to hold stocks for several years, even if the market does not immediately recognize their true value.

Example of Value Investing:

Warren Buffett, one of the most successful investors of all time, is a renowned value investor. He has built his fortune by identifying undervalued companies and holding them for the long term.

2. Growth Investing

Growth investing is an investment strategy that focuses on companies with high growth potential. Growth investors seek out companies that are expected to grow their earnings at a faster rate than the market average.

Key Principles of Growth Investing:

- Revenue Growth: Growth investors prioritize companies with strong revenue growth, as this is a key indicator of future earnings potential.

- Earnings Growth: Growth investors look for companies that are expected to grow their earnings at a rapid pace.

- Innovation: Growth investors often invest in companies that are developing innovative products or services that have the potential to disrupt existing markets.

Example of Growth Investing:

Technology companies such as Amazon and Netflix are examples of growth stocks that have delivered significant returns to investors over the past decade.

3. Income Investing

Income investing is an investment strategy that focuses on generating a steady stream of income from investments. Income investors typically invest in dividend-paying stocks, bonds, and real estate.

Key Principles of Income Investing:

- Dividend Yield: Income investors prioritize stocks with high dividend yields, as this is a measure of the income generated per dollar invested.

- Bond Coupon Rates: Income investors look for bonds with attractive coupon rates, as this is the fixed interest rate paid on the bond.

- Rental Income: Income investors often invest in real estate to generate rental income.

Example of Income Investing:

Real estate investment trusts (REITs) are a popular choice for income investors, as they are required to distribute a significant portion of their earnings to shareholders in the form of dividends.

4. Index Investing

Index investing is an investment strategy that involves tracking a specific market index, such as the S&P 500. Index investors typically invest in index funds or exchange-traded funds (ETFs) that replicate the performance of the index.

Key Principles of Index Investing:

- Diversification: Index funds and ETFs provide instant diversification, as they hold a basket of stocks that represent the index.

- Low Costs: Index funds and ETFs typically have low expense ratios, making them a cost-effective way to invest in the market.

- Passive Management: Index funds and ETFs are passively managed, meaning that they do not attempt to outperform the market.

Example of Index Investing:

The Vanguard S&P 500 ETF (VOO) is a popular choice for index investors, as it provides broad exposure to the U.S. stock market at a low cost.

5. Dollar-Cost Averaging

Dollar-cost averaging is an investment strategy that involves investing a fixed amount of money at regular intervals, regardless of the market price. This strategy can help to reduce the risk of investing a large sum of money at the wrong time.

Key Principles of Dollar-Cost Averaging:

- Regular Investments: Dollar-cost averaging involves investing a fixed amount of money at regular intervals, such as monthly or quarterly.

- Automatic Investing: Dollar-cost averaging can be automated through online brokerage accounts or employer-sponsored retirement plans.

- Long-Term Perspective: Dollar-cost averaging is a long-term strategy that requires patience and discipline.

Example of Dollar-Cost Averaging:

If an investor invests $100 per month in a stock, they will purchase more shares when the price is low and fewer shares when the price is high. Over time, this can help to reduce the average cost per share.

Mastering Risk Management: Essential Strategies for Investors

Risk management is a crucial aspect of investing, as it helps to protect your capital and achieve your financial goals. Here are some essential risk management strategies that every investor should consider:

1. Diversification

Diversification is the practice of spreading your investments across a variety of asset classes, industries, and geographic regions. This can help to reduce the impact of any single investment on your overall portfolio.

Key Principles of Diversification:

- Asset Allocation: Diversify your portfolio across different asset classes, such as stocks, bonds, and real estate.

- Industry Diversification: Diversify your stock holdings across different industries to reduce the risk of being overly exposed to any single sector.

- Geographic Diversification: Diversify your investments across different countries and regions to reduce the risk of being overly exposed to any single economy.

Example of Diversification:

A diversified portfolio might include stocks from various industries, bonds from different issuers, and real estate investments in different geographic locations.

2. Asset Allocation

Asset allocation is the process of determining how to allocate your investments across different asset classes. The optimal asset allocation will depend on your individual circumstances, including your risk tolerance, time horizon, and financial goals.

Key Principles of Asset Allocation:

- Risk Tolerance: Your risk tolerance is a measure of how much risk you are willing to take with your investments.

- Time Horizon: Your time horizon is the length of time you have to invest before you need to access your funds.

- Financial Goals: Your financial goals will influence your asset allocation decisions.

Example of Asset Allocation:

A young investor with a long time horizon and a high risk tolerance might allocate a larger portion of their portfolio to stocks, while an older investor with a shorter time horizon and a low risk tolerance might allocate a larger portion of their portfolio to bonds.

3. Stop-Loss Orders

A stop-loss order is an order to sell a stock when it reaches a certain price. This can help to limit your losses if the stock price declines.

Key Principles of Stop-Loss Orders:

- Set a Stop Price: Determine the price at which you want to sell the stock if it declines.

- Monitor Your Positions: Regularly monitor your positions and adjust your stop-loss orders as needed.

- Consider Volatility: Take into account the volatility of the stock when setting your stop-loss orders.

Example of Stop-Loss Orders:

If an investor buys a stock at $50 and sets a stop-loss order at $45, the stock will automatically be sold if the price declines to $45.

4. Position Sizing

Position sizing is the process of determining how much capital to allocate to each investment. This can help to manage your risk and prevent any single investment from having too large of an impact on your portfolio.

Key Principles of Position Sizing:

- Risk Tolerance: Your risk tolerance will influence your position sizing decisions.

- Investment Size: Determine the maximum amount of capital you are willing to risk on any single investment.

- Portfolio Size: Take into account the overall size of your portfolio when making position sizing decisions.

Example of Position Sizing:

If an investor has a $100,000 portfolio and is willing to risk 2% of their capital on any single investment, they would allocate no more than $2,000 to each position.

5. Regular Portfolio Review

It’s important to regularly review your portfolio to ensure that it is still aligned with your investment goals and risk tolerance. This includes rebalancing your portfolio to maintain your desired asset allocation.

Key Principles of Regular Portfolio Review:

- Rebalance Your Portfolio: Rebalance your portfolio regularly to maintain your desired asset allocation.

- Review Your Goals: Review your financial goals to ensure that they are still aligned with your investment strategy.

- Adjust Your Strategy: Adjust your investment strategy as needed to reflect changes in your circumstances or the market environment.

Example of Regular Portfolio Review:

An investor might review their portfolio annually to rebalance their asset allocation and ensure that their investments are still aligned with their financial goals.

By implementing these risk management strategies, investors can protect their capital and increase their chances of achieving their financial goals.

Crafting Your Financial Future: Long-Term Financial Planning

Long-term financial planning is essential for achieving your financial goals and securing your financial future. Here are some key steps to creating a comprehensive financial plan:

1. Define Your Financial Goals

The first step is to define your financial goals. What do you want to achieve with your money? Do you want to retire early, buy a house, or start a business?

Key Considerations When Defining Your Financial Goals:

- Specific: Make your goals specific and measurable.

- Realistic: Set realistic goals that are achievable given your current financial situation.

- Time-Bound: Set a timeline for achieving your goals.

Example of Financial Goals:

- Retire at age 60 with an annual income of $100,000.

- Buy a house in five years with a 20% down payment.

- Start a business in ten years with $50,000 in startup capital.

2. Assess Your Current Financial Situation

The next step is to assess your current financial situation. This includes evaluating your income, expenses, assets, and liabilities.

Key Considerations When Assessing Your Financial Situation:

- Income: Track your income from all sources.

- Expenses: Track your expenses to identify areas where you can save money.

- Assets: List your assets, including cash, investments, and real estate.

- Liabilities: List your liabilities, including loans, credit card debt, and mortgages.

Example of Assessing Your Financial Situation:

An investor might create a spreadsheet that lists their income, expenses, assets, and liabilities to get a clear picture of their current financial situation.

3. Develop a Budget

A budget is a plan for how you will spend your money. It can help you to track your expenses, identify areas where you can save money, and allocate your resources towards your financial goals.

Key Considerations When Developing a Budget:

- Track Your Expenses: Use a budgeting app or spreadsheet to track your expenses.

- Set Spending Limits: Set spending limits for different categories, such as food, entertainment, and transportation.

- Automate Savings: Automate your savings by setting up automatic transfers to your savings account.

Example of Developing a Budget:

An investor might use a budgeting app to track their expenses and set spending limits for different categories.

4. Create an Investment Plan

An investment plan is a strategy for how you will invest your money to achieve your financial goals. It should take into account your risk tolerance, time horizon, and financial goals.

Key Considerations When Creating an Investment Plan:

- Risk Tolerance: Determine your risk tolerance and allocate your investments accordingly.

- Time Horizon: Consider your time horizon when making investment decisions.

- Financial Goals: Align your investment strategy with your financial goals.

Example of Creating an Investment Plan:

An investor might create an investment plan that allocates a portion of their portfolio to stocks, bonds, and real estate, based on their risk tolerance, time horizon, and financial goals.

5. Monitor Your Progress and Adjust Your Plan

It’s important to monitor your progress towards your financial goals and adjust your plan as needed. This includes reviewing your budget, tracking your investments, and making adjustments to your strategy as your circumstances change.

Key Considerations When Monitoring Your Progress:

- Review Your Budget: Review your budget regularly to ensure that you are on track.

- Track Your Investments: Track your investments to monitor their performance.

- Adjust Your Strategy: Adjust your investment strategy as needed to reflect changes in your circumstances or the market environment.

Example of Monitoring Your Progress:

An investor might review their budget and investment performance quarterly to ensure that they are on track to achieve their financial goals.

By following these steps, you can create a comprehensive financial plan that will help you to achieve your financial goals and secure your financial future.

Frequently Asked Questions (FAQ) About Investing

Here are 10 frequently asked questions about investing, along with detailed answers:

1. What is investing?

Investing is the process of allocating money or capital with the expectation of receiving a future benefit or profit. This can involve purchasing assets such as stocks, bonds, real estate, or other investments.

2. Why should I invest?

Investing can help you grow your wealth over time, achieve your financial goals, and protect your money from inflation. It can also provide a source of income in retirement.

3. What are the different types of investments?

There are many different types of investments, including stocks, bonds, mutual funds, exchange-traded funds (ETFs), real estate, and alternative investments.

4. What is risk tolerance?

Risk tolerance is a measure of how much risk you are willing to take with your investments. It is influenced by factors such as your age, financial situation, and investment goals.

5. What is diversification?

Diversification is the practice of spreading your investments across a variety of asset classes, industries, and geographic regions to reduce risk.

6. What is asset allocation?

Asset allocation is the process of determining how to allocate your investments across different asset classes based on your risk tolerance, time horizon, and financial goals.

7. What is dollar-cost averaging?

Dollar-cost averaging is an investment strategy that involves investing a fixed amount of money at regular intervals, regardless of the market price.

8. What is a stop-loss order?

A stop-loss order is an order to sell a stock when it reaches a certain price to limit your losses.

9. How do I choose an investment advisor?

When choosing an investment advisor, consider their qualifications, experience, fees, and investment philosophy.

10. How often should I review my portfolio?

You should review your portfolio regularly, at least annually, to ensure that it is still aligned with your investment goals and risk tolerance.

Need help navigating the complexities of investing? At CONDUCT.EDU.VN, we understand the challenges individuals face when seeking reliable guidance on investment strategies and financial planning. That’s why we offer a wealth of resources and expert insights to empower you on your financial journey.

Don’t let confusion or uncertainty hold you back from achieving your financial aspirations. Visit CONDUCT.EDU.VN today to access comprehensive information, practical tips, and personalized guidance tailored to your unique needs. Whether you’re a novice investor or a seasoned professional, our platform provides the tools and knowledge you need to make informed decisions and build a secure financial future.

For personalized assistance and expert advice, contact us at:

- Address: 100 Ethics Plaza, Guideline City, CA 90210, United States

- WhatsApp: +1 (707) 555-1234

- Website: CONDUCT.EDU.VN

Take control of your financial future today with conduct.edu.vn!