Financial statements of not for profit organizations are essential for transparency and accountability, and CONDUCT.EDU.VN provides a comprehensive guide to understanding them. By offering a clear roadmap of financial health, these statements, including activity statements and cash flow statements, help organizations, boards, and stakeholders navigate the complex financial landscape. Unlock the secrets to financial clarity with resources from CONDUCT.EDU.VN and ensure compliance through robust accounting practices, budget oversight, and comprehensive financial analysis.

1. Understanding the Importance of Financial Statements for Nonprofits

Financial statements are crucial for not for profit organizations (NPOs). They serve as a roadmap for understanding financial health and ensure accountability to stakeholders. These statements provide a clear overview of how an NPO manages its resources. This insight enables informed decision-making and builds trust with donors and the community.

1.1. Key Benefits of Compiling Financial Statements

Compiling nonprofit financial statements goes beyond merely meeting regulatory requirements. These reports offer a comprehensive overview of an organization’s financial health. This knowledge empowers stakeholders to:

- Ensure Regulatory Compliance: Adhering to government regulations and Generally Accepted Accounting Principles (GAAP) is crucial for maintaining tax-exempt status and legal compliance.

- Enhance Financial Oversight: Financial statements offer a clear snapshot of the organization’s assets, liabilities, and net assets, facilitating better oversight and risk management.

- Support Strategic Planning: By analyzing financial data, organizations can identify trends, forecast future performance, and make informed decisions about resource allocation.

- Attract Funding: Transparent financial reporting builds trust with donors and grantmakers, increasing the likelihood of securing funding and support.

- Improve Accountability: Financial statements demonstrate accountability to stakeholders, including donors, board members, and the community, ensuring responsible use of resources.

- Benchmark Performance: Comparing financial statements over time and against similar organizations allows for benchmarking and identification of areas for improvement.

- Strengthen Internal Controls: The process of preparing financial statements helps identify weaknesses in internal controls and implement measures to prevent fraud and errors.

- Communicate Impact: Financial statements can be used to communicate the organization’s impact to stakeholders, showcasing how resources are being used to achieve its mission.

1.2. Developing a Financial Reporting Policy

A financial reporting policy establishes clear guidelines for creating and distributing financial statements, ensuring transparency and consistency. This policy should outline the roles and responsibilities of individuals involved in the financial reporting process. It should define the frequency of reporting, the types of statements to be prepared, and the distribution channels. A well-defined policy maximizes transparency and accountability. It can also serve as a reference for internal staff and external stakeholders.

Key elements of a financial reporting policy:

| Element | Description |

|---|---|

| Purpose | State the policy’s objective, such as ensuring accurate and transparent financial reporting. |

| Scope | Define who the policy applies to, including staff, board members, and external stakeholders. |

| Roles and Responsibilities | Clearly outline the roles and responsibilities of individuals involved in the financial reporting process. |

| Reporting Frequency | Specify how often financial statements will be prepared (e.g., monthly, quarterly, annually). |

| Types of Statements | List the types of financial statements to be prepared (e.g., statement of activities, balance sheet). |

| Distribution Channels | Describe how financial statements will be distributed (e.g., email, website, board meetings). |

| Approval Process | Outline the process for reviewing and approving financial statements. |

| Compliance | Ensure compliance with GAAP and other regulatory requirements. |

| Review and Update | Establish a schedule for reviewing and updating the policy to ensure it remains relevant and effective. |

2. The Four Major Nonprofit Financial Statements Explained

Most nonprofits compile four main financial statements. Each report offers a different perspective on the organization’s financial health. These statements provide unique insights into various aspects of the NPO’s performance.

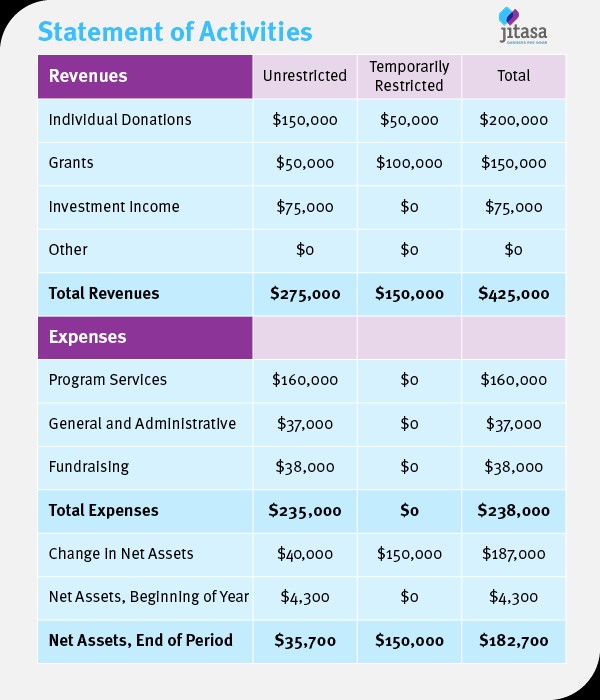

2.1. Statement of Activities: A Deep Dive

The statement of activities is similar to the income statement for for-profit organizations. It provides detailed information about an organization’s transactions. It showcases how expense allocation and revenue generation support the mission.

2.1.1. Key Components of the Statement of Activities

- Revenue: This section breaks down the nonprofit’s funding sources. Common sources include individual donations, grants, earned income (e.g., membership dues), and investment returns. Distinguishing between unrestricted and restricted funds is vital.

- Expenses: Expenses are categorized by function, such as program, administrative, and fundraising costs. This categorization helps assess how resources are allocated toward the mission.

- Net Assets: Net assets are calculated by subtracting total expenses from total revenue. Comparing net assets at the beginning of the fiscal year to the change during the year offers valuable insights.

2.1.2. Understanding Restricted vs. Unrestricted Funds

Distinguishing between unrestricted and restricted funds is essential. Restricted funds must be used for a specific purpose, as agreed with the donor. Unrestricted funds can be allocated to any expense. This distinction highlights the flexibility of the nonprofit’s funding.

2.1.3. Comparing Budget vs. Actual Expenses

Comparing the statement of activities with the operating budget is crucial. It allows for evaluating planned versus actual expenses and revenue generation. This comparison informs more accurate predictions for future budgets.

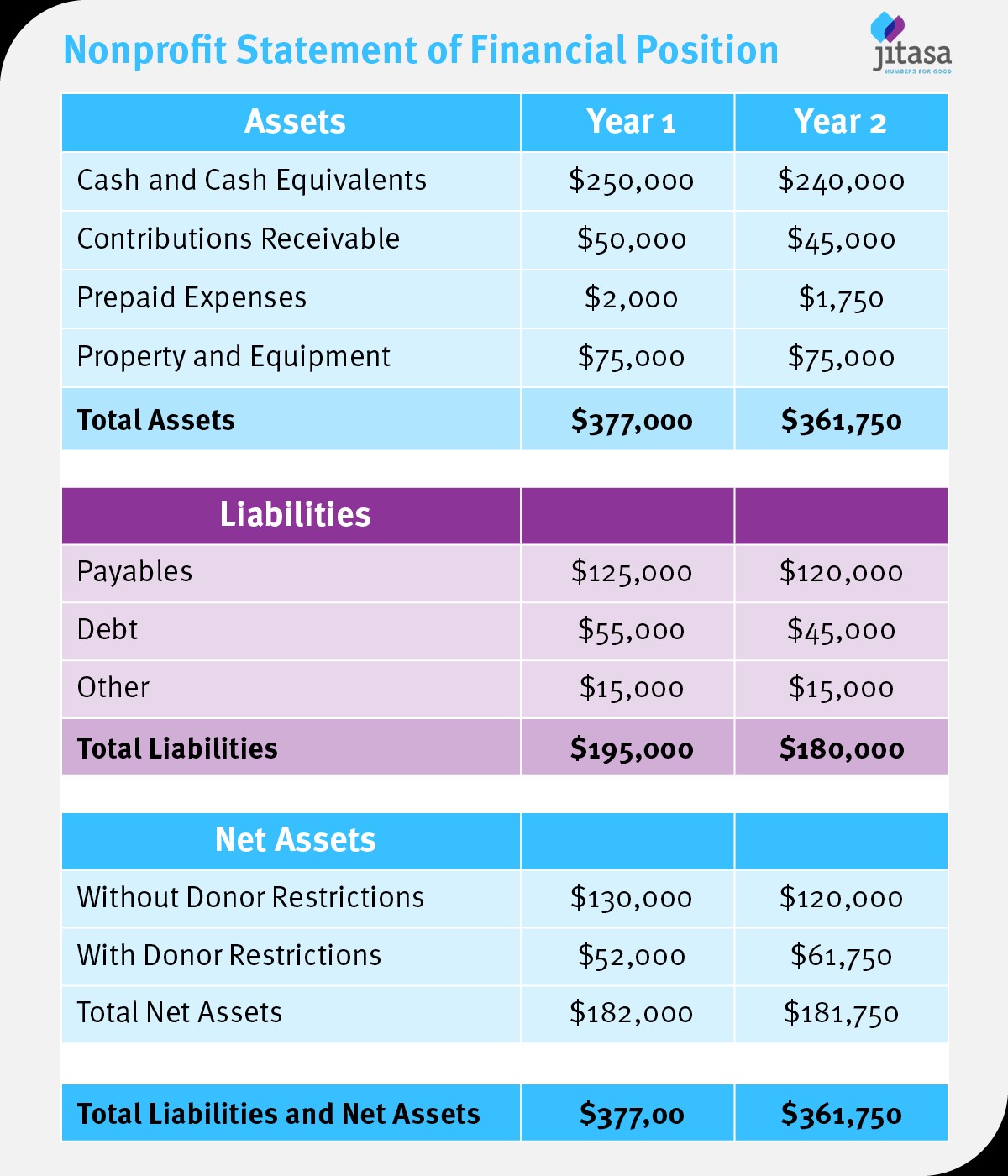

2.2. Statement of Financial Position: A Snapshot of Financial Health

The statement of financial position, also known as the balance sheet, provides a snapshot of an organization’s financial health. It is a crucial document in nonprofit financial audits.

2.2.1. Key Components of the Statement of Financial Position

- Assets: This section lists everything the nonprofit owns, such as cash, accounts receivable, property, and equipment. Assets are listed in order of liquidity.

- Liabilities: Liabilities include everything the nonprofit owes, such as accounts payable, debt, and lease obligations. These are typically organized by due date.

- Net Assets: Net assets are calculated by subtracting total liabilities from total assets. Separate restricted and unrestricted net assets.

2.2.2. Analyzing Assets and Liabilities

Comparing assets and liabilities year-over-year indicates whether financial health is improving. This analysis can help plan for growth. Sufficient cash on hand is necessary to cover operating costs and additional expenses.

2.2.3. Planning for Growth with the Balance Sheet

The balance sheet assists in planning for organizational growth. It helps determine if there are enough liquid assets to support expansion. This insight enables informed decisions about taking on new projects or initiatives.

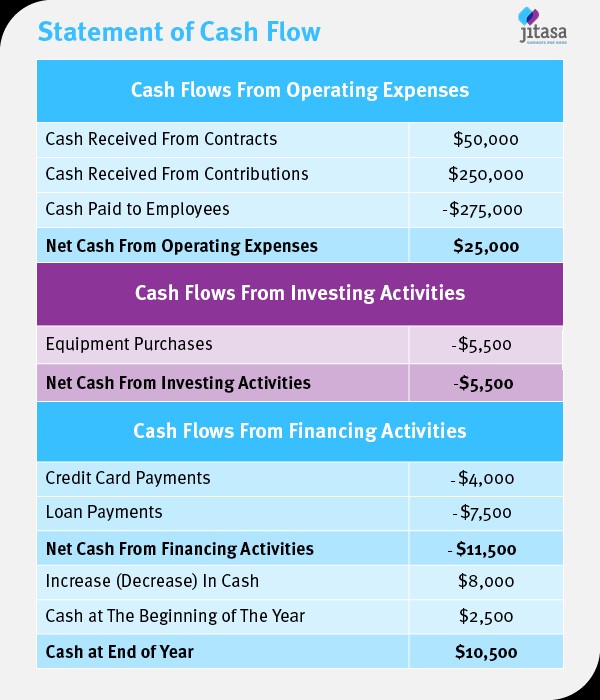

2.3. Statement of Cash Flows: Monitoring Cash Movement

The statement of cash flows shows how cash moves in and out of the organization. It is usually pulled monthly, rather than annually.

2.3.1. Key Components of the Statement of Cash Flows

- Operating Activities: This section includes revenue and expenses from day-to-day activities. Examples include fundraising, contracting, and salary payments.

- Investing Activities: This covers long-term assets, such as purchasing office equipment or opening brokerage accounts.

- Financing Activities: This section includes long-term liabilities, such as borrowing and repayment of debts and endowment funds.

2.3.2. Monitoring Spending and Fundraising

The statement of cash flows helps monitor spending and fundraising monthly. It ensures the organization stays on track with its budget. It also prevents accidental overdrafts.

2.3.3. Ensuring Financial Stability

Monitoring cash flow is vital for ensuring financial stability. Understanding cash inflows and outflows helps manage resources effectively. This proactive approach prevents financial crises and supports sustainable operations.

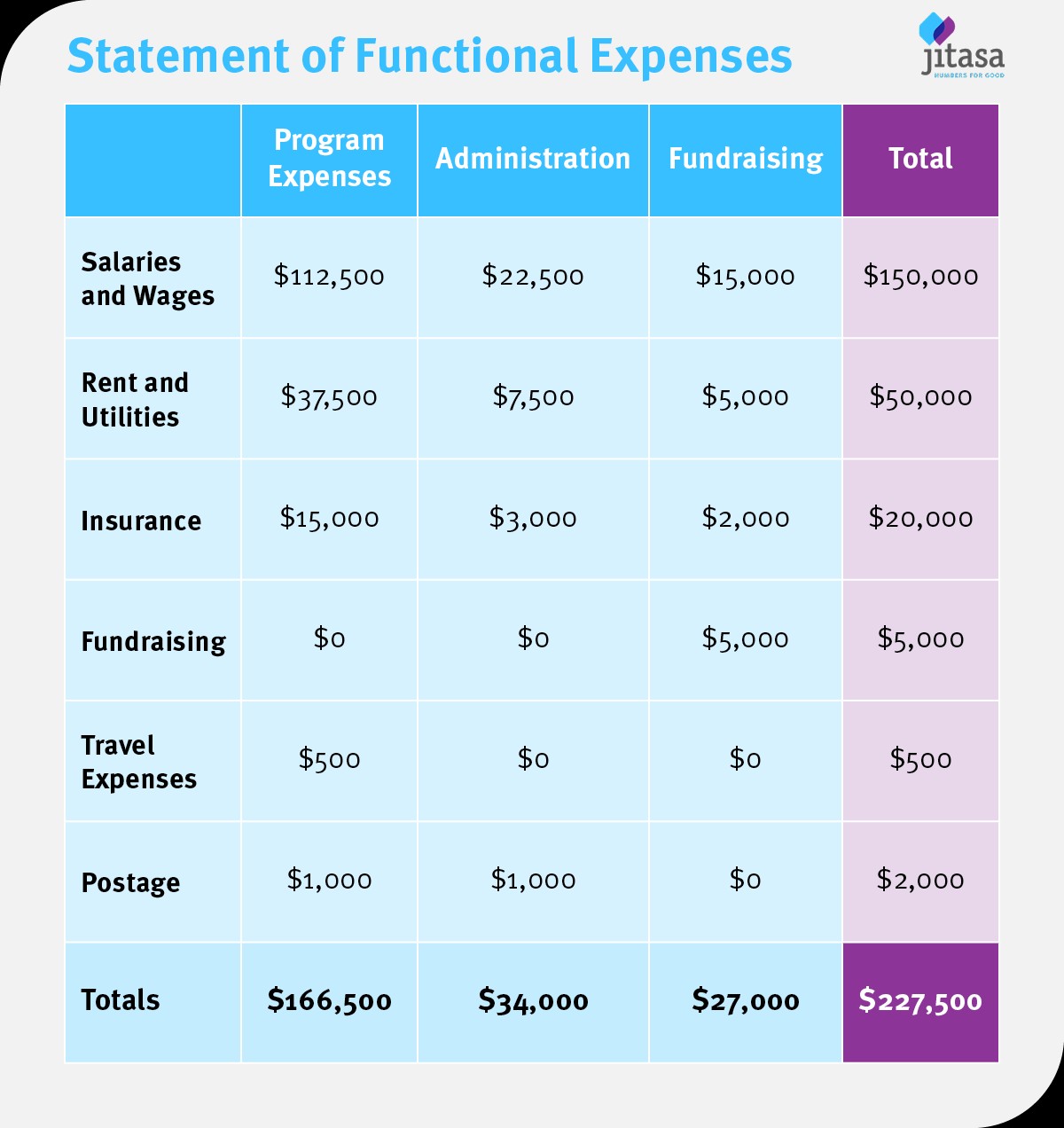

2.4. Statement of Functional Expenses: Understanding Expense Allocation

The statement of functional expenses is unique to nonprofits. It reorganizes costs based on their function in furthering the organization’s mission.

2.4.1. Key Components of the Statement of Functional Expenses

- Program Costs: These are directly cause-related expenses. For example, an environmental organization might include the costs of educational workshops.

- Administrative Costs: These are necessary for day-to-day operations. Examples include staff compensation, rent, and utilities.

- Fundraising Costs: These include expenses for event planning, marketing, and fundraising consultant fees.

2.4.2. Understanding Overhead Expenses

Overhead expenses refer to administrative and fundraising costs combined. While the 65/35 rule (65% toward program expenses, 35% on overhead) is a guideline, the breakdown varies. Reviewing this statement identifies areas to reduce overhead spending.

2.4.3. Preparing for Tax Filings

The statement of functional expenses aids in filing annual tax returns. It provides detailed information needed for Form 990 and its variations. Accurate reporting ensures compliance and transparency.

3. Creating Financial Statements: Best Practices

Creating accurate financial statements requires careful attention to detail. Using the right tools and expertise ensures reliability.

3.1. Utilizing Accounting Software

Accounting software stores all information needed for financial statements. This streamlines the compilation process. Choosing software designed for nonprofits is beneficial.

3.2. Working with a Nonprofit Accountant

Working with a nonprofit accountant ensures accurate and useful financial statements. Outsourcing to a firm like Jitasa provides specialized expertise. This is particularly helpful for organizations without a full-time accountant.

3.3. Step-by-Step Guide to Compiling Financial Statements

Here’s a step-by-step guide to compiling financial statements:

- Gather all financial data: Collect all relevant financial records, including bank statements, invoices, and receipts.

- Organize your data: Categorize your financial data into the appropriate accounts and categories.

- Prepare the statement of activities: Summarize your organization’s revenue and expenses for the reporting period.

- Prepare the statement of financial position: List your organization’s assets, liabilities, and net assets at a specific point in time.

- Prepare the statement of cash flows: Track the movement of cash in and out of your organization during the reporting period.

- Prepare the statement of functional expenses: Allocate your organization’s expenses to program, administrative, and fundraising activities.

- Review and analyze the statements: Carefully review the financial statements to identify trends, assess financial health, and make informed decisions.

- Disclose required information: Ensure all required disclosures are included in the financial statements, such as related party transactions and significant accounting policies.

- Obtain an independent audit: Consider obtaining an independent audit of your financial statements to enhance credibility and transparency.

- Distribute the statements: Share the financial statements with stakeholders, including board members, donors, and the public.

3.4. Ensuring Accuracy and Compliance

Ensuring accuracy and compliance involves several key steps:

- Regular Reconciliation: Reconcile bank statements and other financial records regularly to identify and correct errors.

- Internal Controls: Implement internal controls to prevent fraud and errors. This includes segregation of duties and approval processes.

- GAAP Compliance: Adhere to Generally Accepted Accounting Principles (GAAP) to ensure consistency and comparability.

- Professional Review: Have financial statements reviewed by a qualified accountant or auditor.

- Stay Updated: Stay informed about changes in accounting standards and regulations.

- Documentation: Maintain thorough documentation of all financial transactions.

- Training: Provide training to staff and board members on financial reporting requirements.

- Audit Trail: Establish a clear audit trail to track financial transactions from source to financial statement.

- Software Validation: Regularly validate accounting software to ensure it is functioning correctly.

- Feedback Loop: Establish a feedback loop to address questions and concerns from stakeholders regarding financial reporting.

4. Common Challenges and How to Overcome Them

Nonprofits face unique challenges in financial reporting. Addressing these challenges ensures accurate and transparent reporting.

4.1. Lack of Resources and Expertise

Many nonprofits operate with limited resources and may lack in-house accounting expertise. This can lead to errors and non-compliance.

Solutions:

- Outsourcing: Consider outsourcing accounting functions to a specialized firm like Jitasa.

- Training: Provide training for staff members responsible for financial tasks.

- Volunteers: Utilize skilled volunteers to assist with accounting and financial reporting.

- Software: Invest in user-friendly accounting software that simplifies financial management.

- Consultants: Engage consultants to provide guidance and support on complex accounting issues.

4.2. Complexity of Fund Accounting

Fund accounting can be complex, requiring careful tracking of restricted and unrestricted funds.

Solutions:

- Dedicated Chart of Accounts: Use a dedicated chart of accounts to track different types of funds separately.

- Software Features: Utilize accounting software features that support fund accounting.

- Training: Provide training on fund accounting principles to relevant staff members.

- Regular Audits: Conduct regular audits to ensure proper handling of funds.

- Policies and Procedures: Develop clear policies and procedures for managing restricted funds.

4.3. Ensuring Transparency and Accountability

Maintaining transparency and accountability is crucial for building trust with stakeholders.

Solutions:

- Open Communication: Maintain open communication with stakeholders about financial matters.

- Regular Reporting: Provide regular financial reports to board members, donors, and the public.

- Independent Audits: Conduct independent audits to enhance credibility.

- Online Access: Provide online access to financial information for stakeholders.

- Whistleblower Policy: Implement a whistleblower policy to encourage reporting of unethical behavior.

4.4. Compliance with Regulations

Staying compliant with ever-changing regulations can be challenging.

Solutions:

- Stay Informed: Stay updated on changes in accounting standards and regulations.

- Professional Advice: Seek professional advice from accountants and auditors.

- Compliance Calendar: Maintain a compliance calendar to track important deadlines.

- Software Updates: Ensure accounting software is updated to reflect regulatory changes.

- Internal Reviews: Conduct regular internal reviews to identify and address compliance issues.

4.5. Difficulty in Measuring Impact

Measuring the impact of programs and services can be difficult but is essential for demonstrating value to stakeholders.

Solutions:

- Key Performance Indicators (KPIs): Develop KPIs to measure the impact of programs and services.

- Data Collection: Implement systems for collecting data on program outcomes.

- Stakeholder Feedback: Seek feedback from stakeholders on the impact of programs.

- Reporting on Impact: Report on program impact in financial statements and other communications.

- Logic Models: Use logic models to link program activities to outcomes.

5. Optimizing Financial Management for Long-Term Sustainability

Effective financial management ensures long-term sustainability for nonprofits. Strategic planning and resource allocation are key.

5.1. Budgeting and Forecasting

Budgeting and forecasting are essential tools for financial planning.

Best Practices:

- Realistic Budgets: Create realistic budgets based on historical data and future projections.

- Regular Monitoring: Monitor budget performance regularly and make adjustments as needed.

- Scenario Planning: Conduct scenario planning to prepare for different financial outcomes.

- Stakeholder Input: Involve stakeholders in the budgeting process to ensure buy-in.

- Long-Term Forecasts: Develop long-term financial forecasts to guide strategic planning.

5.2. Diversifying Funding Sources

Relying on a single funding source can be risky. Diversifying funding sources enhances financial stability.

Strategies:

- Grant Writing: Pursue grants from foundations, government agencies, and corporations.

- Individual Donations: Cultivate relationships with individual donors and solicit donations.

- Earned Income: Explore opportunities to generate earned income through fees for services or product sales.

- Fundraising Events: Organize fundraising events to raise money and engage supporters.

- Corporate Sponsorships: Seek corporate sponsorships to support programs and events.

5.3. Investing in Technology

Investing in technology improves efficiency and accuracy in financial management.

Technology Solutions:

- Accounting Software: Implement accounting software to automate financial processes.

- Donor Management Systems: Use donor management systems to track donations and donor relationships.

- Online Payment Processing: Utilize online payment processing to facilitate online donations.

- Cloud Computing: Embrace cloud computing for secure and accessible data storage.

- Data Analytics: Leverage data analytics to gain insights into financial performance.

5.4. Building a Strong Finance Committee

A strong finance committee provides oversight and guidance on financial matters.

Key Responsibilities:

- Reviewing Financial Statements: Review financial statements and provide feedback to management.

- Overseeing the Budget Process: Oversee the budget process and ensure it aligns with strategic goals.

- Monitoring Financial Performance: Monitor financial performance and identify areas for improvement.

- Ensuring Compliance: Ensure compliance with accounting standards and regulations.

- Providing Financial Advice: Provide financial advice and guidance to the board and management.

5.5. Developing a Reserve Policy

A reserve policy ensures the organization has sufficient funds to cover unexpected expenses and maintain operations during times of financial stress.

Key Considerations:

- Target Reserve Level: Determine the appropriate target reserve level based on the organization’s risk profile.

- Funding Sources: Identify funding sources for building the reserve.

- Investment Strategy: Develop an investment strategy for managing reserve funds.

- Withdrawal Policy: Establish a policy for withdrawing funds from the reserve.

- Regular Review: Review the reserve policy regularly and make adjustments as needed.

6. Examples of Financial Statements in Practice

Real-world examples illustrate the practical application of financial statements.

6.1. Case Study: Environmental Conservation Organization

An environmental conservation organization uses its statement of activities to track donations, grants, and program expenses. It ensures funds are allocated effectively to conservation projects.

6.2. Case Study: Social Services Agency

A social services agency uses its balance sheet to monitor assets and liabilities. It manages cash flow to support daily operations and expand services.

6.3. Case Study: Arts and Culture Nonprofit

An arts and culture nonprofit uses its statement of cash flows to manage fundraising events and track expenses. It ensures financial stability and supports artistic programs.

7. Frequently Asked Questions (FAQ) About Nonprofit Financial Statements

Addressing common questions clarifies the intricacies of nonprofit financial statements.

Q1: What are the four basic financial statements for a nonprofit?

A1: The four basic financial statements are the statement of activities, statement of financial position, statement of cash flows, and statement of functional expenses.

Q2: Why is the statement of functional expenses unique to nonprofits?

A2: The statement of functional expenses is unique because it categorizes expenses by program, administrative, and fundraising activities, reflecting the organization’s mission-related activities.

Q3: What is the difference between restricted and unrestricted funds?

A3: Restricted funds are designated for a specific purpose by the donor, while unrestricted funds can be used for any organizational purpose.

Q4: How often should a nonprofit prepare financial statements?

A4: Nonprofits should prepare financial statements at least annually, with the statement of cash flows often prepared monthly.

Q5: What is the 65/35 rule, and how does it apply to functional expenses?

A5: The 65/35 rule suggests that nonprofits should allocate at least 65% of their funding to program expenses and no more than 35% to overhead, although this is a guideline and varies by organization.

Q6: Why is it important for nonprofits to compare their budget to their actual expenses?

A6: Comparing the budget to actual expenses helps nonprofits evaluate their financial performance and make informed decisions for future budgeting.

Q7: What role does accounting software play in preparing financial statements?

A7: Accounting software automates the collection, organization, and reporting of financial data, streamlining the preparation of financial statements.

Q8: Why might a nonprofit choose to outsource its accounting needs?

A8: Nonprofits may outsource accounting to access specialized expertise, ensure accuracy, and reduce the burden on internal staff.

Q9: How does a strong finance committee contribute to effective financial management?

A9: A strong finance committee provides oversight, reviews financial statements, monitors budget performance, and ensures compliance with regulations.

Q10: What is a reserve policy, and why is it important for nonprofits?

A10: A reserve policy ensures that the organization has sufficient funds to cover unexpected expenses and maintain operations during financial stress, promoting long-term stability.

8. Resources for Further Learning

Numerous resources are available for those seeking to deepen their understanding of nonprofit financial statements.

8.1. Online Courses and Webinars

Online courses and webinars offer in-depth instruction on nonprofit accounting and financial reporting.

8.2. Professional Associations

Professional associations like the American Institute of Certified Public Accountants (AICPA) provide resources and guidance for nonprofit accountants.

8.3. Government Publications

Government publications from the IRS and other agencies offer regulatory guidance on nonprofit financial reporting.

9. The Role of CONDUCT.EDU.VN in Promoting Ethical Financial Practices

CONDUCT.EDU.VN plays a vital role in promoting ethical financial practices within not for profit organizations. By providing comprehensive resources and guidance, CONDUCT.EDU.VN supports transparency, accountability, and sound financial management.

9.1. Accessing Expert Guidance

CONDUCT.EDU.VN offers access to expert guidance on nonprofit financial reporting. This includes articles, templates, and tools for creating accurate and compliant financial statements.

9.2. Ensuring Accountability

The resources available on CONDUCT.EDU.VN help nonprofits ensure accountability to stakeholders. This builds trust and supports long-term sustainability.

9.3. Building a Culture of Compliance

CONDUCT.EDU.VN promotes a culture of compliance with accounting standards and regulations. This reduces the risk of errors and fraud.

Financial statements are essential for the health and sustainability of not for profit organizations. Understanding these statements and implementing best practices ensures transparency, accountability, and effective resource management. For more detailed information and expert guidance, visit CONDUCT.EDU.VN at 100 Ethics Plaza, Guideline City, CA 90210, United States, or contact us via Whatsapp at +1 (707) 555-1234.

Navigating the complexities of financial reporting can be challenging, but with the right resources and expertise, your nonprofit can achieve financial excellence. Explore the comprehensive guides and support available at CONDUCT.EDU.VN to ensure your organization thrives. Don’t let financial reporting complexities hold you back – visit conduct.edu.vn today and empower your nonprofit with the knowledge and tools it needs to succeed.